SHADOW BANKING

MARK-TO-MARKET LEVERAGE

The Basics

Leverage is the ratio of total assets to equity that a firm has on its balance sheets.

Mark-to-market accounting is a set of accounting standards where asset prices are valued at current market prices/values. This is contrary to normal accounting practices where assets on firms’ balance sheets are valued at historical costs, where the value of the asset is set at the value at the time of the purchase.

Firms, like banks and other financial institutions, use leverage as a tool in order to make loans to their customers (i.e. fractional reserve banking) and to increase their profits.

Mark-to-market accounting is a set of accounting standards where asset prices are valued at current market prices/values. This is contrary to normal accounting practices where assets on firms’ balance sheets are valued at historical costs, where the value of the asset is set at the value at the time of the purchase.

Firms, like banks and other financial institutions, use leverage as a tool in order to make loans to their customers (i.e. fractional reserve banking) and to increase their profits.

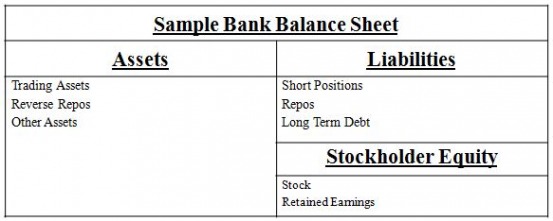

Basic Banking Balance Sheet Structure

Note: Assets = Liabilities + Stockholder Equity

Net Capital Rule (2004)

The net capital rule deals with capital requirement regulations regarding how much of a haircut investment banks must apply to their various tradable securities. Those haircut values are used to find the value of “net capital” needed to pay out their liabilities in case they go out of business/bankrupt. The values reached for the haircuts were normally based on values determined at market prices.

In 2004, the Securities and Exchange Commission issued a ruling that exempted all investment banking firms, with at least $5 billion in assets from the previous ruling and allowed the investment banks to compute their haircuts based on historical data. The changing in computation of haircuts lowered the haircut amounts and freed up vast amounts of capital for the company.

When the capital was freed up following the 2004 SEC Rule change, many investment banks began to increase the amount of debt instruments that they were issuing. This resulted in increased leverage ratios for the investment banks. Leverage ratios allows for potential higher profits, but they also present higher risks of default when crises occur.

In 2004, the Securities and Exchange Commission issued a ruling that exempted all investment banking firms, with at least $5 billion in assets from the previous ruling and allowed the investment banks to compute their haircuts based on historical data. The changing in computation of haircuts lowered the haircut amounts and freed up vast amounts of capital for the company.

When the capital was freed up following the 2004 SEC Rule change, many investment banks began to increase the amount of debt instruments that they were issuing. This resulted in increased leverage ratios for the investment banks. Leverage ratios allows for potential higher profits, but they also present higher risks of default when crises occur.

Leverage Ratios, Investments Banks, and the Net Capital Rule

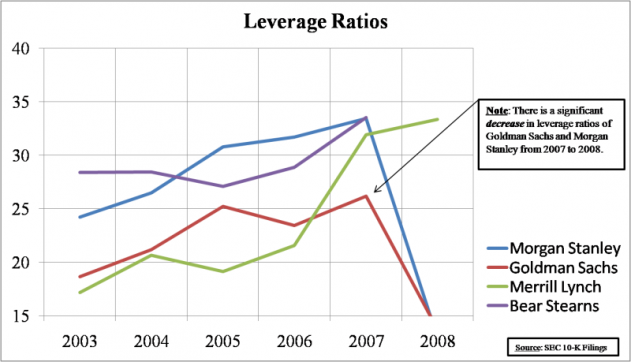

The most significant problem that arose during the financial crisis of 2008 was the increasingly high leverage ratios of investment firms throughout the global financial system. The graph shown here is an illustration of the leverage ratios that four major investment banks had from 2003 to 2008.

Of the four investment firms that are shown on the graph, only two of the firms survived the financial crisis: Goldman Sachs and Morgan Stanley. The two firms that survived the financial crisis of 2008 significantly reduced their leverage ratios from 2007 to 2008.

Of the four investment firms that are shown on the graph, only two of the firms survived the financial crisis: Goldman Sachs and Morgan Stanley. The two firms that survived the financial crisis of 2008 significantly reduced their leverage ratios from 2007 to 2008.

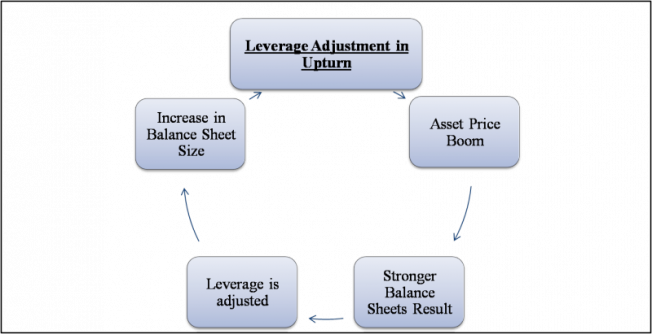

Leverage Adjustment in Upturn

In an asset price boom, banks mark their asset values up as they increase in value which makes their balance sheets look favorable. They are also able to write-up huge profits from those asset price increases. In order to keep those profits growing, they take on more leverage. Many argue that the subprime mortgage asset bubble was a result of this cycle.

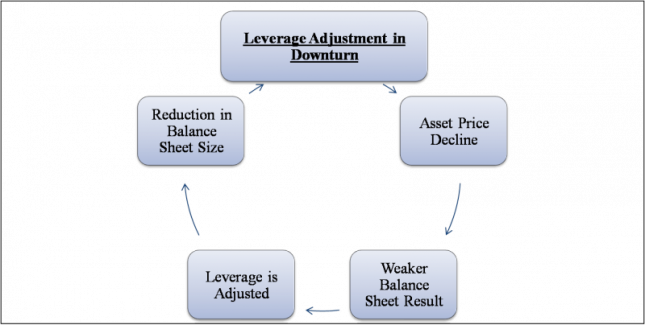

Leverage Adjustment in Downturn

When asset prices decline, the quality of the bank's balance sheet become weaker and the begin the process of "deleveraging". This process usually includes holding more capital on their books. This becomes a problem because they are not lending that money and people who are looking to get loans have a harder time acquire the credit they need.

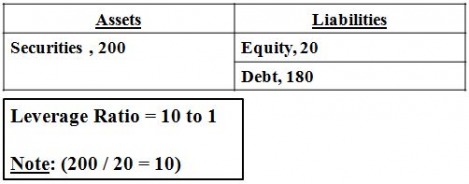

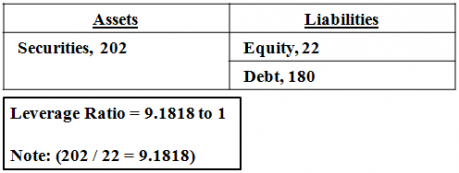

Example - Mark-to-Market Accounting and Balance Sheet Adjustments

Bank Balance Sheet

Note: On balance sheets, the Total Assets must equal Total Liabilities and Stockholder Equity

Leverage Adjustment as a Result of an Asset Price Increase of 1 %

When asset prices go up, the bank's leverage goes down and they must issue more debt in order to bring their leverage ratio back up to where it was previously. This creates a cycle/incentive to take on more debt in order to keep their leverage ratio up and maximize their profits.